by Claudia Segre

https://www.huffingtonpost.it/blog/2026/06/21/news/loro_non_compra_la_pace-22185709

Gold is back in the spotlight amid wars, geopolitical tensions, and inflation fears. Despite recent price declines, central banks and emerging economies are increasing their reserves, transforming the precious metal from a mere safe-haven asset into a strategic security tool.

21 June 2026 at 14:43

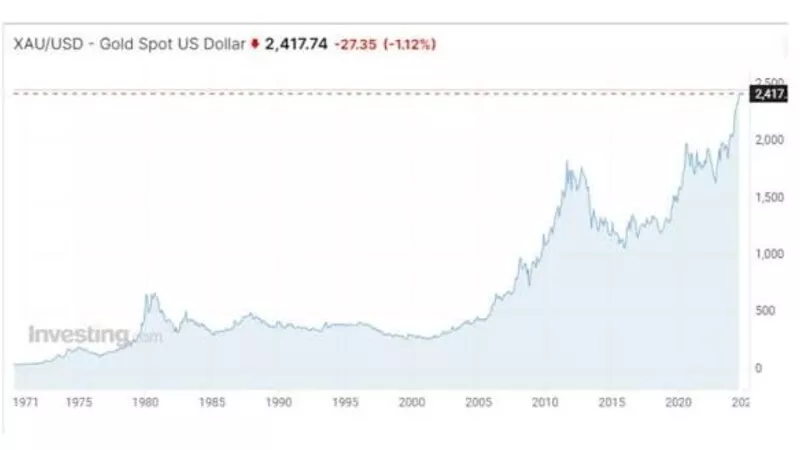

If the price of gold rises, this not only signals periods of nervousness in the financial markets but also affects global confidence in its future as a store of value. Gold has returned to the limelight in recent months as wars, trade tensions, political instability, fears of inflation, and rivalry between major powers have restored it to the role it has always played in times of uncertainty: that of a haven. But as the conflict in the Middle East continues to escalate and the United States and China vie for the global balance of power, gold has fallen to its lowest level since the start of the year. This appears to be a contradictory trend. However, gold’s behaviour is never linear.

Geopolitical crises don’t always drive inflation to record highs. But if the markets begin to fear a return of inflation, so do interest rates. And since gold pays neither dividends nor interest, a stronger dollar or higher bond yields may initially make it less attractive. This is the question investors are asking themselves today: Is this simply a correction, like last autumn, or is there something more structural at play? To answer this question, we need to look beyond the price of gold and consider what central banks are buying and selling. Indeed, for at least four years, the official gold market has been the driving force behind global demand for gold, and not just for speculative purposes.

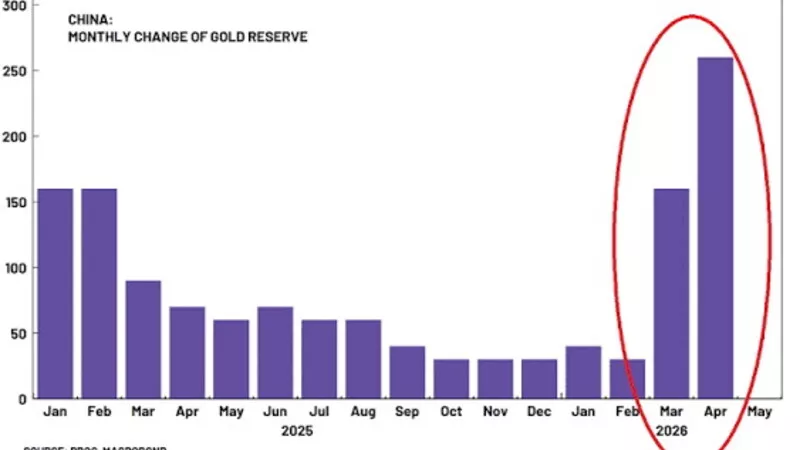

China is the clear leader in this phase. In May, China purchased around 10 tonnes of gold, the highest monthly volume since January 2025. Beijing has been buying gold for nineteen consecutive months, the longest streak in recent years: official reserves have reached around 2,332 tonnes, equivalent to almost 9 per cent of the country’s total foreign exchange reserves. There is more to these figures than just finance: they have geopolitical implications. China still holds dollar-denominated assets and is not abandoning the US currency, which remains the backbone of international trade. But it is gradually diversifying certain strategic assets. In the wake of Russia’s freezing of part of its reserves in 2022, several emerging nations have begun to regard geopolitical risk as a constant factor in reserve management.

Gold is a financial asset that no other asset can match. It does not depend on the existence of a government, a bank, or an international payment system. For this reason, it once again serves as a form of insurance against sanctions, conflicts, and economic fragmentation. And if we compare the situation in the West, the scale of the problem becomes clear. The United States, Germany, Italy, and France still hold some of the largest gold reserves: Italy ranks third globally with nearly 2,452 tonnes. But whilst Western economies are keeping their holdings largely unchanged, countries such as China, Poland, India, and Uzbekistan are adding to their reserves with a consistency not seen for decades. This does not mean that the US dollar will cease to be the benchmark currency or that its importance will diminish. The notion of rapid de-dollarisation is misguided because no other market today has the depth, liquidity, and absorption capacity of the US Treasury market.

We are at a stage where countries are seeking greater strategic autonomy without losing any of the benefits of the existing system. The behaviour of Chinese citizens also tells us something. Demand for jewellery is not yet strong due to high prices. Demand for gold bars, coins, and gold-linked financial instruments is growing. And the precious metal is increasingly seen as a haven for family wealth, in the wake of the property crisis and unstable, highly volatile stock markets. Of course, there are also signs of caution: in May, Chinese gold ETFs were delisted from the market, and wholesale demand has fallen. The market could face a fresh wave of volatility in the short term. But the bigger picture tells a different story. Record public debt, persistent geopolitical tensions, transforming value chains, and a growing emphasis on economic security are changing the way states think about their reserves. Against this backdrop, gold is no longer simply a hedge against inflation or a refuge from financial crisis: it has once again become a component of national security.

And in fact, this could be the most significant change of all. For years, gold has been regarded as a relic of the old monetary systems. The world’s oldest metal is once again playing a role we thought had been rendered obsolete in the age of artificial intelligence, hybrid wars, and technological rivalries. It does not buy peace, nor does it resolve conflicts. But it is also a better measure than ever of the confidence that governments, institutions, and citizens have in the stability of the future. And so it has returned to the spotlight, shining brighter than ever.