by Claudia Segre

BLOGGERS’ CORNER. Climate risk is no longer merely a reputational issue, but a prudential risk, with direct implications for credit, capital, and financial stability.

24 March 2026 at 14:32

The European Central Bank has fined Crédit Agricole, ordering it to pay over €7.5 million for “climate-related” non-compliance. This is not merely a story of banking supervision, but a sign that fits into an increasingly contradictory global context, where the climate transition coexists with a return to energy and security priorities, partly undermining the momentum of the so-called “green revolution”.

The sanction relates to a delay in assessing the materiality of climate and environmental risks: an aspect that appears purely technical, but is in fact central. For the ECB, climate risk is no longer merely a reputational issue, but a prudential risk, with direct effects on credit, capital, and financial stability.

And it is precisely here that the first point for reflection emerges: whilst European finance is being called upon to integrate climate considerations into risk models, the global macroeconomic scenario seems to be moving in the opposite direction.

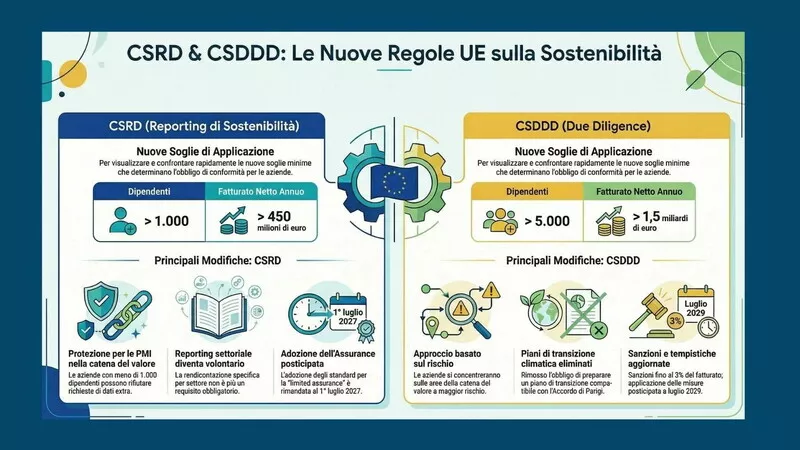

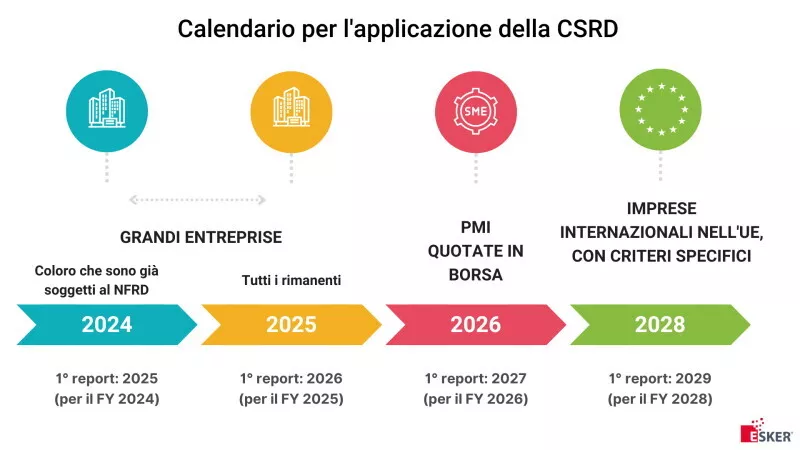

In recent months, market volatility, the resurgence of geopolitical tensions, and the impact of wars on energy prices have brought energy security concerns back to the forefront. In Asia, several countries have increased their reliance on coal to ensure continuity of production. In the United States, the Inflation Reduction Act continues to support the transition, but with a strongly industrial and domestic focus, rather than a regulatory one. In Europe, however, the regulatory framework is becoming increasingly stringent, with the launch of the CSRD and the CSDDD, which impose high standards of transparency, governance, and accountability.

This creates a clear paradox: on the one hand, growing regulatory pressure on the European financial system; on the other, a global context that is slowing down – or at least reshaping – the trajectory of the green transition.

In this scenario, the ECB’s move takes on a significance that goes beyond the individual case. It is not so much an exemplary punishment as an enforcement measure: ‘periodic penalty payments’ serve to encourage compliance, not to impose retroactive sanctions. But the message is clear: the time for gradual adaptation is over.

European supervision has followed a clear path: from the 2020 guidelines to the 2022 climate stress tests, right through to the operational deadlines of 2023–2024. Today, we are entering a different phase, in which shortcomings are no longer tolerated. And the data show this: in the ECB test, around 65% of banks revealed serious shortcomings in climate risk management, whilst a large proportion of exposures remain concentrated in high-emission sectors.

The issue, therefore, is no longer whether climate risk is relevant, but how and how quickly it must be integrated into banking models.

Here, a second tension arises, less visible but equally significant: that between technical capability and regulatory expectations. Banks still report data gaps, particularly regarding Scope 3 emissions and the geolocation of assets. Furthermore, climate scenario models remain complex and poorly standardised. However, for the ECB, uncertainty can no longer be an excuse. So here is the central question: are we facing a warning signal or a caution against the usual opportunism? Probably both.

It is a warning signal because it indicates that climate risk is now an integral part of financial stability. Failing to manage it properly could result in more defaults, write-downs of collateral, and the deterioration of portfolios. In other words, the climate is having a direct impact on banks’ balance sheets.

But it is also a warning. At a time when the ESG narrative risks being sidelined by geopolitical urgencies, the ECB is urging market participants to avoid communication shortcuts or strategic delays. The issue of greenwashing, in fact, remains in the background, alongside the risks of litigation and loss of credibility.

An international comparison reinforces this interpretation. Europe is opting for a regulatory and prudential approach, which aims to internalise climate risks within the financial system. The United States favours incentives and industrial policies. Asia, in some cases, adopts a more pragmatic approach, focused on energy security and growth.

Three different models, reflecting different priorities.

Against this backdrop, the ECB’s decision can be interpreted as an attempt to stay the course at a time of uncertainty. Not an ideological acceleration, but a reaffirmation of consistency: if climate risk is material, then it must be measured, managed, and integrated. The real challenge, however, remains unresolved. Because the transition is not just about the rules, but also about the ability to align finance, the real economy, and the geopolitical context.

And today, more than ever, this alignment appears fragile. With the major banking scandals now behind us, the path to righteousness still appears uneven. It is paved with stumbling blocks that bring to light a structural difficulty: that of banks fully reclaiming a social role. A role that, during the pandemic, seemed to have been rediscovered — as a lever for stability and support for the real economy — but which is now once again being put to the test. Climate risk, in this sense, is not merely a technical challenge: it is the litmus test of a credibility that remains unfulfilled.